Askeladden Capital Shares Plan to Maximize Shareholder Value, Including Specific Operational Improvements Based on Extensive Primary Research

Transdigm’s May 2025 Acquisition of Public Aerospace Component Company Servotronics At 274% Premium Highlights Potential to Unlock Value at AstroNova Through Comprehensive Evaluation of Strategic Alternatives

CEO Greg Woods and Lead Independent Director Richard Warzala Were Colleagues In the 1990s; Long-Standing Relationships May Compromise Board Independence

AstroNova Has Suffered Severe and Persistent Shareholder Value Destruction Under Five Long-Tenured Board Members; Recent Statements Demonstrate Lack of Commitment to Shareholder Value

FORT WORTH, TX / ACCESS Newswire / May 22, 2025 / Askeladden Capital Management LLC

To AstroNova Shareholders,

I write to you as the portfolio manager of Askeladden Capital (collectively, “we”), which on behalf of our clients is the largest shareholder of AstroNova, owning approximately 9.2% of the shares. We recently filed our definitive proxy statement for the upcoming annual shareholder meeting scheduled for July 9th. You will soon receive these materials by mail and electronically through your broker.

The company callously suggests that you “disregard and discard” Askeladden’s GOLD proxy card.1 We make no such recommendation about the company’s card.

Instead, we encourage you to make your own decision about who has the better plan, motivation, and capability to deliver value for all long-suffering shareholders of AstroNova. We encourage you to compare AstroNova’s recent financial results and long-term track record of shareholder value destruction with Askeladden’s rigorous analysis, including the plan we present below. We encourage you to speak to AstroNova’s management and Board as well as the Askeladden nominees, and ask each of us detailed, candid questions. In fact, on June 12th at 11 AM ET, we plan to host a virtual town hall meeting for AstroNova shareholders to interact directly with our nominees. More details will follow, but for now, please save the date.

If and when elected, we will work tirelessly to maximize the value of your investment. We will solicit and incorporate your feedback about how to improve AstroNova. We do not have a monopoly on good ideas, and sincerely look forward to hearing yours.

This letter has two sections:

-

Askeladden’s plan to maximize value at AstroNova, including a clear explanation of the research backing the plan, and how our nominees’ specific and relevant expertise is critical to executing this plan. A very comparable transaction from earlier this week, Servotronics, highlights the potential value at AstroNova with better leadership.

-

Analysis of the shareholder value destruction that has occurred under the tenure of current directors Mr. Quain, Mr. Woods, Mr. Warzala, Ms. Schlaeppi, and Mr. Michas, with emphasis on longstanding relationships among certain of these Board members that calls into question their independence and objectivity. We also address some of the recent misleading claims made by these Board members, providing shareholders with important context, from the company’s own disclosures, that the company omitted.

SECTION 1: ASKELADDEN’S PLAN TO MAXIMIZE VALUE AT ASTRONOVA

1.1 Background to the Plan

AstroNova’s recent letter to shareholders falsely states “[Mr. Patel] has failed to provide concrete or additive ideas to unlock value for AstroNova.”2 In fact, Askeladden has engaged with AstroNova on numerous occasions since 2023, seeking to understand the root causes of performance challenges and suggest responses.

In March, when we began to express our concerns and suggestions more forcefully, the company eventually simply stopped responding to our emails rather than attempting to engage with us. We then reluctantly began this proxy contest. The company’s proxy statement discloses that it has already spent $200,000 of shareholder money and anticipates a total expenditure of $1,000,000.3 Not once did the company even attempt to avoid such expenditure by addressing our concerns privately, even though we repeatedly requested them to do so. The company’s own proxy materials disclose that on March 21, 2025, when I submitted the nomination packet at company headquarters, “Mr. Patel requested to have a cup of coffee with [Chief Financial Officer] Mr. DeByle, and Mr. DeByle declined.” 4 Therefore, we humbly submit that a more accurate version of this statement might read: “AstroNova has failed to engage with Askeladden’s concrete and additive ideas to unlock value.”

Before publicly presenting a detailed plan, we took the time to conduct thorough due diligence of AstroNova’s operations and competitive position – something we believe is the fiduciary duty of a public-company Board, and something we believe the incumbent Board failed to do prior to consummating the MTEX acquisition. AstroNova recorded a $13.4 million impairment charge on MTEX less than a year after purchasing it for $18.7 million in cash and assuming certain MTEX debt, and discontinued 70% of the company’s product portfolio.5

Askeladden has researched AstroNova since 2016 and continuously been a 5% shareholder since 2020. Recently, we have developed an even deeper and broader understanding of AstroNova’s business by speaking to fifteen individuals with directly relevant expertise. We sought to understand the root causes of AstroNova’s challenges, as well as industry best practices.

These interviews have been extremely informative. For example, CEO Greg Woods frequently touts the “AstroNova Operating System” in conference calls and presentations, including referencing it during the most recent quarterly call in April 2025 as the path to fixing MTEX and driving strong returns on investment.6 Yet a former AstroNova employee who worked for the company for over four years, who managed a key integration project and was subsequently hired into Director / VP of Operations positions at two other companies, stated, verbatim:

“I don’t remember the AstroNova Operating System per se, which means that it didn’t stick out significantly to me in my career. I’m not going to say it was nothing, but it certainly wasn’t memorable.” 7

Other individuals whom we interviewed had backgrounds including, but not limited to:

-

Managers at printhead technology providers such as Memjet and Epson who directly interacted with AstroNova (one also directly interacted with MTEX);

-

C-level executives and key leaders at industrial printing peers such as Domino and Markem-Imaje, who oversaw significant growth or transformation of those businesses;

-

A former sales representative and former sales executive at AstroNova, and a current customer whom they served;

-

The principal of a private equity firm which thoroughly evaluated MTEX as a potential investment, as well as a former MTEX employee directly reporting to MTEX CEO Eloi Ferreira at the time of AstroNova’s acquisition

In the coming weeks, we will publish more comprehensive analysis of AstroNova’s performance and the best path forward based on these expert insights, with direct excerpts from transcribed interviews available to subscribers of platforms such as Tegus and In Practise.

Our research leads us to believe that AstroNova lacks a culture of accountability, has a dated business strategy in need of significant modernization, is overly reliant on its plan to utilize MTEX’s technology, and is missing key opportunities to better reach and serve its customers.

Our plan will leverage our nominees’ specific and relevant expertise to address the various issues that have arisen repeatedly in our research. We aim to move AstroNova’s strategy closer to best practices successfully utilized by peers. Unlike AstroNova’s existing management and Board, who seem resistant to feedback, we will remain data-driven, nimble, and open to new ideas.

Below is our three-part framework.

An important caveat: We are seeking five out of the six board seats up for election this year. Thus, if only one or two of the Askeladden nominees should be elected, there can be no guarantee that those directors would be able to implement the actions that Askeladden believes are necessary to unlock shareholder value. Whatever the outcome, each of the Askeladden nominees would, in elected, act as a fiduciary for shareholders and seek to work with other members of the Board to evaluate all opportunities to enhance shareholder value.

1.2: First 60 Days: Implement Culture of Accountability, Upgrade Executive Talent, and Improve Margins and Cash Conversion

Given AstroNova’s margin degradation since FY2024, limited availability under its revolving credit facility,8 and the volatile macroeconomic environment, our immediate priority during the first 60 days will be driving rapid improvement in gross and EBITDA margins as well as cash conversion, to maximize free cash flow generation. We will also seek to upgrade talent throughout the organization wherever needed, promoting or hiring individuals with a demonstrated history of excellence in rapidly meeting or exceeding targets.

We will implement an incentives-driven culture of accountability to drive operating results and shareholder value. Immediate priorities will include but not be limited to the following:

-

Directors will meet with AstroNova’s lender to understand its concerns and discuss plans to pay down debt and create headroom on our line of credit;

-

Shorten the cash cycle and reduce working capital by negotiating substantially better payables and receivables terms with vendors and customers and reduce inventory levels.

-

Develop and implement a 26-week cashflow forecast to micromanage costs and preserve working capital.

-

Directors will meet with large customers and suppliers to understand their concerns

-

A/B test price increases, aiming to determine price elasticity and maximize margin dollars as well as return on capital employed;

-

Assess and reprioritize marketing expenditures. This will start with calculation of cost per lead generated, conversion rate, return on advertising spend (ROAS), lifetime value to customer acquisition cost (LTV/CAC), and other relevant metrics to evaluate the effectiveness of sales and marketing expenditures. Based on this analysis, we will rebalance marketing expenditures, reducing spending on trade shows and reallocating those funds to search engine optimization (SEO), search engine advertising (SEA), and other forms of digital marketing, shifting spending to channels with the highest quantifiable ROI.

-

Thoroughly review all major cost categories, reduce and defer non-essential expenditures such as travel and executive perks,

-

Institute stricter controls including requiring CEO or CFO approval for all consulting, and related expenses;

-

Audit customer and product-level profitability to determine and administer minimal contribution standards for margins and returns on capital employed

-

Streamline the sales organization, institute processes to avoid competing against channel partners / distributors, and allocate sales resources to the highest-value activities, shifting low-value activities to other channels such as e-commerce.

1.3: Next 100 Days: Identify Highest-ROI Improvement Opportunities

AstroNova faces many challenges after years of mismanagement. While the company certainly needs some disruption to improve its results, it’s impractical and unwise to immediately and simultaneously address all potential issues we may identify. AstroNova is a small company, and we don’t want to unnecessarily stress the organization’s capacity for change.

Furthermore, some potential initiatives, such as consolidation of the manufacturing footprint, would take time and require investment.

Therefore, we will emphasize “low hanging fruit” – quick wins with limited up-front investment. We seek to maximize cash generation or margin improvement in the short term, without overwhelming the organization’s capacity to manage change or disrupting other initiatives.

Once the company is generating more substantial cash flows and has reduced its indebtedness, we will work to address the remaining issues and focus on longer-term strategic initiatives.

We will review:

-

Product lines and market positioning – in which product categories and customer segments do we have a right to win, and do so profitably? Evaluate all aspects of the business through the lens of return on invested capital (ROIC) and focus investment in ROIC-maximizing areas, prioritizing returns and profitability over absolute size.

-

Go-to-market strategy: conduct a deeper and more thorough segmentation and re-evaluation of the go-to-market strategy, including the appropriate methods (direct, channel, e-commerce) and sales team organization and compensation for each product line and customer type. Consider hiring a specific executive with relevant prior experience to manage and build the company’s global channel strategy.

-

Customer strategy: center the organization around the customer to maximize the lifetime value of the installed base; deepen customer relationships and aim to become a trusted partner rather than just a supplier. Recognizing that labels are a small component of customers’ costs but a critical part that can prevent shipments and revenue recognition, aim to provide a superlative quality and reliability experience and compete on value and service rather than price. Implement “Voice of Customer” strategies, particularly for new product introductions, and institute and incentivize against key health metrics such as Net Promoter Score and customer retention (measured in both units and dollars).

-

Analyze operating footprint: analyze make-vs-buy decisions for components that are currently (or could possibly be) vertically integrated using existing manufacturing capacity, and conversely any components that could be outsourced to reliable supply partners. Evaluate facilities and determine which products can most profitably be produced where.

-

Evaluate production equipment, particularly in areas such as electronics and printed circuit boards, to determine areas where modest capital investments might drive tangible improvements in operating costs and product quality.

-

Identify opportunities to monetize owned real estate, including working with the lender to determine their views on a sale-leaseback of the Chicago and West Warwick properties to reduce debt.

-

Evaluate integration plans at MTEX and determine the best path forward for maximizing the value of that asset.

1.4: Ongoing: evaluate strategic alternatives and, when appropriate, execute on risk-adjusted value-maximizing opportunities

Based on our research and analysis, we think that AstroNova’s current corporate structure is inefficient. A portion of AstroNova’s unallocated corporate overhead attributable to public-company costs would be significantly reduced or eliminated in a transaction with a private purchaser or a larger public company. Furthermore, we think the Aerospace and Product Identification businesses have negligible overlap in customers and at best limited overlap in underlying technology. Both segments are individually much smaller than many of their peers. Many aerospace and printing companies have substantially larger revenues and thus a greater ability to leverage technology and marketing spend over a broader customer base.

Given AstroNova’s low liquidity and current depressed market valuation, we think a transaction or series of transactions resulting in the sale or merger of the company may represent the most efficient way to maximize shareholder value. After years of shareholder value destruction, fiduciary duty demands that the Board – whether the incumbents or our nominees – thoroughly investigate strategic alternatives. We will prioritize developing and implementing a viable standalone business strategy as a public company, and pursue whichever path maximizes shareholder value. It is critical for the company to at least be aware of the private-market value for the business as a whole, and its individual segments, and weigh that against its valuation in the public markets to determine the appropriate path forward. (For the latter scenario, tax considerations would factor into our assessment of the value-maximizing strategy).

We note Servotronics (SVT), a global designer and manufacturer of servo controls and other components for aerospace and defense applications, announced a merger with large aerospace manufacturer Transdigm (TDG) for $110 million in cash on May 19, 2025. That price is almost identical to AstroNova’s entire enterprise value as of May 20, 2025.9,10 This all-cash transaction represents a 274% premium to Servotronics’ share price at the prior close. For the fiscal year 2024, Servotronics generated $44.9 million in revenue with only $8.2 million in gross profit and less than $1 million in Adjusted EBITDA.11

Meanwhile, for its FY2025 ended a month later, AstroNova’s Test and Measurement segment (subsequently renamed Aerospace) generated a slightly higher $48.9 million in revenues with a much higher $11.1 million in segment operating profit. It seems reasonable to assume that a buyer evaluating these two businesses side by side would assign a higher valuation to AstroNova Aerospace given its modestly higher revenues and substantially higher profits. In other words (and apart from any tax considerations), that would imply that if AstroNova Aerospace was sold at a similar value, AstroNova could pay off all its debt and return cash to shareholders equivalent to roughly the current share price. Shareholders would then still own the entire Product Identification segment, with slightly over $100 million in annual revenues generated each of the past three fiscal years, which is clearly worth substantially more than the zero or even negative value implied if Servotronics’ valuation is applied to AstroNova Aerospace.12

While the Servotronics transaction is merely one data point, it demonstrates the potential value if AstroNova focuses on rapid improvements and evaluates strategic alternatives, rather than doubling down on a strategy promoted by the value-destroying incumbent CEO and Board.

1.5: Our Directors Have Specific and Relevant Experience To Execute the Plan

Shawn Kravetz. Mr. Kravetz has relevant experience as a change agent under similar circumstances. He joined the Board of Nevada Gold & Casinos, Inc. as a large shareholder frustrated by performance, including a recent acquisition. He served from 2016 until Nevada Gold was sold in 2019, including Chairman of the Corporate Governance and Nominating Committee. Mr. Kravetz was recently nominated for election to the Board of publicly-traded Spruce Power Holding Corporation by the company’s Nominating and Governance Committee.13

Jeff Sands. As Mr. Sands discusses in his book, “Corporate Turnaround Artistry: Fix Any Business in 100 Days,” he has successfully used techniques included in our plan to restore profitability at numerous businesses, including some merely weeks away from lender-forced liquidation. He has won the Turnaround Management Association “Turnaround of the Year” award three times. Mr. Sands has successfully worked with businesses such as a $100M supplier of aerospace components to Boeing (~2x the size of AstroNova’s Aerospace segment), as well as complex and capital-intensive businesses such as steel and pharmaceuticals. Given AstroNova’s significant recent decline in profitability and elevated inventory balances, Mr. Sands’ experience in driving rapid cash flow improvement is extremely relevant.

Ryan Oviatt. Mr. Oviatt has extensive experience – as CFO, CEO, and Board Member of Profire – of managing an industrial products business for margin and cash flow in the highly cyclical energy market. AstroNova’s relatively more advantaged capital-light business model, with substantial recurring revenues driven by a large installed base, provide a solid foundation to build on. Mr. Oviatt managed a team that used techniques such as automation of manual processes and key administrative functions, customer outreach, and performance-based incentive compensation programs designed to instill a sense of ownership throughout the company.

Boyd Roberts. Mr. Roberts was the youngest member of the executive team at Franklin Covey (FC) and has integrated and substantially grown an acquired division, with ownership of full P&Ls and high employee net promoter scores. Mr. Roberts has extensive experience with Franklin Covey’s customer-focused recurring-revenue business model. Mr. Roberts is fluent in Portuguese. His linguistic and cultural strengths uniquely qualify him to address the challenging MTEX acquisition, which we believe has suffered due to a cultural mismatch between the labor force at its facility in Porto in northern Portugal, and AstroNova’s American business culture.14

Samir Patel. As AstroNova’s largest shareholder, who has researched the business since 2016, I am deeply familiar with the company’s ongoing (flawed) strategy, contrary to the company’s misleading assertion that the company will be damaged by a new Board “unacquainted with recent decision-making.” 15 I will ensure that AstroNova’s operational and capital allocation decisions consistently maximize shareholder value.

1.6: Strategic Alternatives Qualifications

Our nominees, are, collectively, extremely qualified to evaluate whether AstroNova can generate more shareholder value through a standalone strategy, or through the sale of the company in whole or part. They have participated in the consummation of successful transactions.

-

Mr. Sands has been involved in the sale of numerous private companies.

-

As CEO and Board Member at public company Profire Energy, Mr. Oviatt helped lead the acquisition of two small private companies and the successful sale of Profire to a strategic public-company buyer, CECO Environmental. After multiple rounds of negotiation, Profire successfully achieved a final offer price 27.5% higher than CECO’s original offer, and an all-cash deal rather than the original offer of 75% cash and 25% stock. This final offer represented a 60.3% premium to Profire’s volume-weighted average share price over the 30 days prior to the Board approving the merger.16

-

Mr. Kravetz was involved in the sale of Nevada Gold & Casino to a strategic buyer, Maverick Casinos.17

-

Mr. Roberts has extensive experience with mergers and acquisitions from deal sourcing and negotiating through integration in his various roles at Franklin Covey, including Vice President of Corporate Development.

SECTION 2: THE CASE FOR CHANGE: WHY ASTRONOVA’S EXISTING BOARD SIMPLY ISN’T GOOD ENOUGH

2.1: Track Record of Poor Performance

We believe that AstroNova’s recent shareholder letter demonstrates that the existing Board is not serious about addressing shareholder value. To start, their letter claims that the election of new directors “presents a significant danger of damaging… employees’ morale.”18 That statement is difficult to take seriously when on March 20, 2025, the company announced “the reduction of approximately 10% of the Company’s global workforce, primarily in the PI [Product Identification] segment.” Poor management and governance has necessitated downsizing – hardly a boon for employee morale. A more profitable and growing AstroNova would benefit employees as well as shareholders by providing opportunities for bonuses and career growth.

The Company’s most recent shareholder letter, similarly, states that “our stock price has recovered from its low of $6.15 during the global pandemic, to its recent price of $9.00.” It is misleading and disingenuous for the Board and executives to compare today’s price to the depths reached during the pandemic – when travel, and life as we know it, was shut down on a global basis. In our view, focusing on the pandemic-low stock price, while ignoring a decade-plus track record of shareholder value destruction, highlights incumbents’ callous attitude towards owners.

We think much more relevant comparison points are:

-

AstroNova’s total shareholder return under the tenure of CEO Greg Woods and each of the other directors serving prior to 2025;

-

Shareholder returns since the disastrous MTEX acquisition in May 2024.

We further think it is important to compare AstroNova’s performance to relevant peers. Given AstroNova’s two distinct segments (Aerospace and Product Identification) and the absence of direct publicly-traded competitors, identifying an exact like-for-like peer group is challenging. As benchmarks for comparison, we have selected:

-

the iShares Micro-Cap ETF (IWC) and iShares Small-Cap ETF (IWM) to reflect AstroNova’s market capitalization,

-

the iShares US Aerospace & Defense ETF (ITA) to reflect AstroNova’s Aerospace segment,

-

two U.S. companies offering industrial and label printing solutions (Brady Corporation, BRC and Zebra Technologies, ZBRA) to reflect AstroNova’s Product Identification segment.19 (We note that AstroNova’s Chief Technology Officer, Michael Natalizia, joined AstroNova in 1986, but worked as a Senior Engineer for Zebra Technologies from 2000 – 2005. We have identified two other AstroNova employees whose LinkedIn profiles cite prior roles at Brady Corporation or Zebra Technologies.20,21)

None of these benchmarks is individually perfect. However, they collectively demonstrate that companies of similar size, producing similar products, or serving similar end markets, have delivered substantially greater returns over relevant time periods. We believe AstroNova’s incumbent Board is touting their resumes and their previous accomplishments elsewhere because their track record of total shareholder return at AstroNova is horrific.

Measured through the record date for the annual meeting (May 15, 2025), AstroNova’s total shareholder return (TSR) has severely underperformed each of these peers since each of the following milestones:

-

Mitch Quain joins Board – August 24, 2011

-

Greg Woods becomes CEO – February 1, 2014

-

Richard Warzala joins Board – December 6, 2017

-

Yvonne Schlaeppi joins Board – April 3, 2018

-

Alexis P. Michas joins Board – June 17, 2022

-

MTEX Acquisition announced – May 9, 2024

|

TSR Since Mitchell Quain joins Board (August 24, 2011) |

TSR since Greg Woods Named CEO (February 1, 2014) |

TSR since Richard Warzala Joins Board (December 6, 2017) |

TSR since Yvonne Schlaeppi Joins Board (April 3, 2018) |

TSR since Alexis Michas Joins Board (June 17, 2022) |

TSR Since AstroNova Announces MTEX (May 9, 2024) |

|

|

AstroNova (ALOT) |

40.1% |

-28.3% |

-37.0% |

-43.5% |

-24.1% |

-51.1% |

|

iShares Micro-Cap ETF (IWC) |

228.8% |

81.6% |

37.8% |

35.8% |

18.2% |

1.8% |

|

iShares Small-Cap ETF (IWM) |

264.2% |

115.3% |

52.5% |

51.6% |

31.0% |

2.3% |

|

iShares US Aerospace & Defense ETF (ITA) |

629.0% |

266.4% |

101.7% |

86.4% |

86.5% |

27.1% |

|

Brady Corporation (BRC) |

294.0% |

254.6% |

125.1% |

132.7% |

82.8% |

26.1% |

|

Zebra Technologies (ZBRA) |

772.6% |

442.80% |

183.3% |

113.4% |

3.4% |

-5.7% |

|

Peer Median Performance |

294.0% |

254.6% |

101.7% |

86.4% |

31.0% |

2.3% |

|

ALOT Underperformance vs. Peer Median |

-253.9% |

-282.9% |

-138.7% |

-129.9% |

-55.1% |

-53.3% |

|

ALOT Underperformance vs. Worst Peer |

-188.7% |

-109.9% |

-74.8% |

-79.3% |

-27.6% |

-45.3% |

This analysis demonstrates that AstroNova has dramatically underperformed its peers during the tenure of CEO Greg Woods and each of the directors who have enabled him.22 Excluding Mr. Michas and Mr. Nevin, the other four directors have had tenures of 7 to 14 years – and what have they accomplished for shareholders during this time? No matter when they joined the board, AstroNova’s share price today shows that the Company has substantially underperformed the worst-performing peer, let alone the median or the best-performing peer. ALOT has a negative absolute return under the tenure of Mr. Woods, Mr. Warzala, Ms. Schlaeppi, and Mr. Michas.

2.2 Long-Standing Relationships May Compromise Board Independence and Objectivity

We think an intertwined web of long-term relationships among four of the five longer-serving Board members may explain their reluctance to hold Mr. Woods accountable:

-

Mitchell Quain has been a director since 2011 and was thus part of the Board that appointed Mr. Woods CEO.

-

Lead Independent Director Richard Warzala and Mr. Woods both worked at Buffalo, NY based American Precision Industries (API) in the mid to late 1990s, through its subsequent acquisition by Danaher. Mr. Woods’ final role was President, API Controls while Mr. Warzala’s was President, API Motion.23,24

-

From 2015 – 2017, Alexis P. Michas served on the Board of Allied Motion Technologies (the former name of Allient, Inc), where according to AstroNova’s proxy statement, Mr. Warzala has served as CEO since 2009 and Chairman since 2014.25

AstroNova has been at the bottom of the selected benchmarks during the tenure of each of these directors. Shareholders have suffered for long enough. The time for substantial Board refreshment is now.

2.3 Lack of Organic Growth

The company’s own recent words demonstrate its lack of commitment to shareholder value. The company trumpets its growth in revenues and operating income but omits important facts, thereby misleading shareholders:

“The strategic repositioning of our Company in the last eleven years has translated into a much-improved financial profile. Since fiscal 2014, AstroNova has delivered a 7.5% compound annual growth rate (“CAGR”) in revenue. While operating income was a loss of $8.6 million in fiscal 2025, adjusted operating income1 over the eleven-year period grew at a 12.2% CAGR.”26

FY2014 is a particularly favorable starting point: GAAP operating income nearly halved from $2.9 million in FY2013 to $1.5 million in FY2014.27 The company sold its medical division, Grass Technologies, on January 31, 2013, for $18.6 million in cash, depressing operating income the following year.28

Further, its Form 10-K for FY2024 notes “at the end of fiscal 2014, we had approximately $27 million of cash, cash equivalents and investments held for sale.” The balance sheet listed no debt and only $11.4 million in total liabilities, primarily comprised of working capital items such as accounts payable, accrued compensation, and other accrued expenses. Additionally, the company discloses that it spent $6.7 million to purchase the ruggedized printer product line from Miltope on January 22, 2014 – so this acquisition contributed virtually nothing to FY2014 results given it was only owned for a week, but would have benefited FY2015 results.

11 years later, for FY2025, AstroNova reports $5.1 million of cash and equivalents29, with $46.6 million of total indebtedness, and $69.8 million of total liabilities. In other words, AstroNova today has over $41 million in net debt, whereas it had over $27 million in net cash when Mr. Woods became CEO, along with nearly $7 million spent on an acquisition merely a week prior. That balance sheet swing of approximately $75 million is essentially equivalent to AstroNova’s entire market capitalization today. We further note that according to Form 10-K disclosures over the past 11 years, AstroNova has spent roughly $92 million on acquisitions since the start of January 2014.30

|

Date |

Purchase Price (Millions) |

Notes |

|

|

Miltope |

January 22, 2014 |

$6.7 |

|

|

RITEC |

June 18, 2015 |

$7.4 |

|

|

TrojanLabel |

February 1, 2017 |

$9.1 |

|

|

Honeywell |

September 28, 2017 |

$29.6 |

$14.6 million in up-front cash, $15.0 million in minimum royalty obligations, and additional excess royalty obligations – we are only including the minimum obligations and the cash payment |

|

Astro Machine |

August 4, 2022 |

$17.0 |

|

|

MTEX |

May 9, 2024 |

$22.1 |

$18.7 million cash purchase price and $3.4 million of MTEX debt assumed. |

|

Total |

$91.9 |

What did the company get in return for spending this shareholder capital? While the company does not always disclose financials for individual transactions, the company disclosed that it purchased Astro-Machine for $17.1 million in cash in August 2022; the business generated $22 million in revenue with “mid-teens” operating margins – implying over $3 million in operating income or a purchase value of less than 6x operating income.31

If AstroNova had spent the remaining $75 million at double the valuation paid for Astro-Machine, the company would have been able to add over $6 million of operating income, in addition to the $3 million delivered by Astro-Machine, for a total of $9+ million in additional operating income.

Yet the company’s own table discloses that non-GAAP operating income grew from $1.86 million as of FY2014 to $6.6 million in FY2025.32 Total operating income is thus less than what the company should have been able to acquire for $92 million. Operating income has grown less than $5 million in 11 years, compared to the over $9 million that they should have generated by deploying over $90 million in shareholder capital, to say nothing of organic growth they should have generated along the way.

Even if we exclude the ongoing MTEX losses, this suggests that AstroNova has not generated organic growth or profitability improvement from the many acquisitions it has consummated, and in fact has likely seen deteriorating results in the businesses that it has purchased.

So Mr. Woods has indeed grown revenues and income by spending the cash he inherited, then borrowing more – but he has not created shareholder value in the process. Most recently, the disastrous MTEX acquisition – which added significant debt while reducing earnings and cash flow due to ongoing losses at MTEX – resulted in breached debt covenants, forcing AstroNova to seek a waiver and deferred debt payment schedule from the lender, which was subsequently granted.33 AstroNova’s letter to shareholders fails to mention this precarious financial situation.

2.4 Guidance for FY 2026 Still Below FY2024 Actual Results

Meanwhile, although the company is pointing to its expected growth in FY2026, it neglects to mention that it still expects to be behind where it was in FY2024, even with the costly addition of MTEX.

In FY2025, excluding MTEX (i.e., organically), revenue declined to $147.1 million from $148.1 million in FY2024, and operating income declined to $8.2 million from $8.8 million in FY2024.34Including MTEX but excluding the associated goodwill impairment of $13.4 million less than a year(!) after purchase, AstroNova’s revenue increased from $148.1 million in FY2024 to $151.3 million in FY2025, but operating income decreased from $8.8 million in FY2024 to $4.8 million in FY2025, with MTEX losing over $3 million even without the goodwill impairment.

The company boasts of its guidance of $160 to $165 million in revenue with 8.5% to 9.5% Adjusted EBITDA margins, but even if the company achieves the high end of this guidance, it would only generate $15.7 million in Adjusted EBITDA. For FY 2024, it had $17.6 million of Adjusted EBITDA excluding restructuring and retrofit-related items.35 So despite the costly MTEX acquisition, FY2026 results – even at the high end of guidance – would still fall below FY2024 results.

2.5 MTEX Strategy Faces Many Pitfalls

Finally, the company’s strategy to fix the ailing Product Identification segment appears primarily based on the roll-out of new MTEX technology. We have multiple reasons to believe this is an unsound approach. First, it is worth asking: if this technology is so revolutionary, why has MTEX been unable to sell it profitably so far as part of AstroNova, and why was it necessary to discontinue 70% of the MTEX product portfolio and write off 70% of the purchase price less than a year after consummation of the acquisition?36

We believe MTEX was an immature business for which AstroNova vastly overpaid, with newly-developed products which may have reliability issues. A former Senior Vice President at Memjet – who worked closely with both AstroNova and MTEX – observed the following (note that “Trojan” refers to AstroNova’s TrojanLabel product line, specifically the T2-C):

The purchase price paid by AstroNova for MTEX, I compare that with the solidity of the Astro Machine business, which was a similar order of magnitude purchase price […] when I compare that to MTEX and the fact that the business was significantly less mature, the fact that one minute, MTEX is making an ATOM, Trojan two Compact competitor, then moves into an overprinter, then starts selling UV cabinets for clothing during COVID, to then switch back to trying to extend into more expensive, higher markets in terms of the packaging segment, it seemed like a very rich price, given that less maturity and with a very fluid product portfolio. […]

Just one last thing to mention about MTEX. I think there was also a lot of disquiet in the marketplace in terms of their ability, that they grew very fast and then to support products. There were a number of situations where I heard from OEMs and resellers who would struggle to get post-sales support when there were issues with the technology.

When it’s one or two, that can be very much a customer-specific scenario. When you get a little bit more of a regular point of feedback around that, then it raises some more questions. I think I’ve read some online comments about the support experience. I think that was another area that was questionable for me around their potential ability.37

We note that AstroNova is no stranger to quality issues, with ink quality issues that were not resolved until the end of FY2024 after originally surfacing at the end of FY202238, despite assurances that it would be a short term fix.39 We question why AstroNova’s Board agreed to pay such a robust price for MTEX – a price they had to write down by 70% relative to cash outlay less than a year later – despite MTEX’s history and seemingly foreseeable potential issues. What kind of due diligence did the Board conduct prior to this acquisition? If they missed these issues, what might they still be missing about the technology upon which AstroNova’s future products apparently rely?

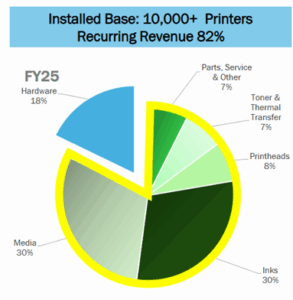

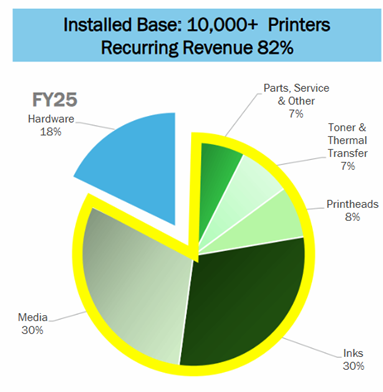

Second, even if AstroNova can work through these reliability concerns, the company’s claim that it is at an “inflection point… positioned to drive meaningful growth and profitability”40 needs additional context. The Company’s own earnings presentation discloses that the company’s Product Identification segment has an installed base of 10,000+ printers with 82% recurring revenue, and only 18% of FY25 revenue attributable to hardware / the sales of new printers.41

While exact lifespans vary depending on the model, maintenance, and usage, we believe inkjet printers and label printers have a lifespan of 3 – 7 years, with well-maintained models potentially lasting longer.42 AstroNova’s large installed base and recurring revenue base is clearly one of the company’s greatest strengths, but it also means that a new technology rollout cannot be accomplished quickly. Even if this new technology proves to be reliable and achieves product-market fit – as of yet unproven – and even if it benefits margins – also as-of-yet unproven, given that MTEX has reported substantial operating losses even excluding its goodwill impairment – it could be 2030 or beyond before the existing installed base is fully replaced by this new technology. We believe that a more balanced focus including other levers to improve performance would be much more advantageous.

Conclusion

Under the 11-year tenure of CEO Greg Woods and the tenure of each of the four Board members nominated prior to 2025, AstroNova shareholders have suffered substantial value destruction, including a loss of almost 50% of the value of their investment over the year following the MTEX acquisition.

The incumbent Board has stood idly by. The current CEO and Board fail to take advantage of AstroNova’s inherently attractive qualities, such as its large base of recurring revenue. AstroNova needs more talented management, a better strategy aligned with industry best practices, and a stronger governance framework focused on accountability to results and shareholder returns. Finally, the company’s Board owes shareholders a comprehensive strategic alternatives process, to determine whether a transaction, or series of transactions, would provide a superior risk-adjusted outcome for shareholders relative to remaining public.

Our slate of nominees has the skills, experience, and motivation to effectively address each of these challenges. We look forward to rolling up our sleeves and working to maximize the value of your investment.

I encourage all shareholders, large or small, to reach out to me directly if they wish to share their perspectives on AstroNova and discuss how our nominees can set the company on a path to a brighter future. I have committed to not accepting any cash or stock compensation for serving as a director (only customary reimbursement of expenses.) My sole motivation is the restoration of shareholder value on behalf of my clients and all long-suffering AstroNova shareholders.

I look forward to speaking with you individually and earning your vote. As a reminder, on June 12th at 11 AM ET, we plan to host a virtual town hall meeting for AstroNova shareholders to interact directly with our nominees. More details will follow, but please save the date.

This filing, and future filings, will also be made available to shareholders after dissemination on EDGAR via our website: https://www.askeladdencapital.com/astronova/

These documents will also be available at no cost at www.sec.gov.

Sincerely,

Samir Patel

samir@askeladdencapital.com

(682) 553-8302

Samir Patel, Askeladden Capital Management LLC, Jeff Sands, Shawn Kravetz, Ryan Oviatt and Boyd Roberts (collectively the “Participants”) filed a definitive proxy statement and accompanying proxy card with the SEC on May 20, 2025, as amended on May 21, 2025, to be used in soliciting proxies in connection with the 2025 annual meeting of shareholders (the “Annual Meeting”) of AstroNova, Inc. (the “Company”). All shareholders of the Company are advised to read the Proxy Statement and other documents related to the solicitation of proxies, each in connection with the Annual Meeting, by the Participants, as they contain important information, including additional information related to the Participants, including a description of their direct or indirect interests by security holdings or otherwise. The Proxy Statement and an accompanying GOLD proxy card will be furnished to some or all of the Company’s stockholders and is, along with other relevant documents, available at no charge on the SEC website at http://www.sec.gov, or by contacting Samir Patel at 1452 Hughes Road, Suite 200 #582, Grapevine, TX, 76051.

1“AstroNova Sends Letter to Shareholders Highlighting Growth Strategy and Strength of Board.” May 19, 2025. https://investors.astronovainc.com/news/press-releases/press-release-details/2025/AstroNova-Sends-Letter-to-Shareholders-Highlighting-Growth-Strategy-and-Strength-of-Board/default.aspx

2“AstroNova Sends Letter to Shareholders Highlighting Growth Strategy and Strength of Board.” May 19, 2025. https://investors.astronovainc.com/news/press-releases/press-release-details/2025/AstroNova-Sends-Letter-to-Shareholders-Highlighting-Growth-Strategy-and-Strength-of-Board/default.aspx

3AstroNova definitive proxy statement filed May 19, 2025. Page 4.

4AstroNova definitive proxy statement filed May 19, 2025. Page 10.

5AstroNova Form 10-K for FY2025. Impairment discussed on page 11; purchase price discussed on page 15.

6Examples include: Q4 FY2025 Earnings Call Transcript – April 14, 2025. Three Part Advisors Southwest Ideas Conference – November 21, 2024. Q4 FY 2024 Earnings Call Transcript – March 22, 2024. Sidoti Micro Cap Investor Conference – January 18, 2024. East Coast IDEAS Investor Conference – June 21, 2023.

7Transcript: “Former Quality Manager at AstroNova Believes Aggressive Change and Leadership are Key for Competitive Edge.” May 6, 2025 – Tegus by AlphaSense.

8AstroNova FY2025 Form 10-K filed April 15, 2025. Page 27 notes only $3.3 million in availability at year-end on the company’s $25 million revolving credit facility. The financial tables show reduction in profitability metrics such as operating income and cash provided by operations.

9“Transdigm to Acquire Servotronics For About $110 million.” May 19, 2025. https://www.nasdaq.com/articles/transdigm-acquire-servotronics-about-110-mln

10 Per data sources such as Seeking Alpha, ALOT shares closed at $9.12 on May 20, 2025. The company’s recent definitive proxy statement, filed May 19, 2025, discloses a recent sharecount of approximately 7.6 million shares, for a market cap of approximately $69 million as of today. AstroNova’s Form 10-K filed April 15, 2025 discloses $20.9 million outstanding on the revolving credit facility, $6.1 million in current long-term debt, $0.6 million in short-term debt, and $19 million in long-term debt, for a total of $46.6 million in gross debt. The same Form 10-K disclosed $5 million of cash and equivalents, making net debt $41.6 million. The sum of $41 million and $69 million is approximately $110 million.

11Form 10-K for Servotronics SVT filed March 17, 2025.

12AstroNova Form 10-K for FY2025, filed April 15, 2025. Page 24.

13 Spruce Power Holding Corp Definitive Proxy, page 10.

14“The American work culture focuses on ambition… in Portugal, there is a more collective approach to work and less pressure… [people] tend to place greater importance on personal well-being, family time, and life outside of work.” LXUS (Corporate Relocation service provider.) https://www.lxusportugal.com/blog-lxusportugal/cultural-comparison-between-the-usa-and-portugal

15Letter accompanying AstroNova’s definitive proxy statement, filed May 19, 2025.

16Profire Energy (PFIE) SC14D9 dated December 3, 2024. Section “Background of the Offer and the Merger” on pages 9 – 16. https://www.sec.gov/Archives/edgar/data/1289636/000110465924124898/tm2429518-1_sc14d9.htm

17Maverick Casinos Announces Sales/Merger Agreement with Nevada Gold. September 2018.

https://www.maverickgaming.com/uncategorized/maverick-casinos-announces-sales-merger-agreement-with-nevada-gold/

18AstroNova Sends Letter to Shareholders Highlighting Growth Strategy and Strength of Board.” May 19, 2025. https://investors.astronovainc.com/news/press-releases/press-release-details/2025/AstroNova-Sends-Letter-to-Shareholders-Highlighting-Growth-Strategy-and-Strength-of-Board/default.aspx

19Brady Corp’s form 10-K filed September 6, 2024 discusses “product identification” as one of its primary product categories, including labeling for applications such as work in process, brand protection, finished product and asset tracking, and healthcare identification. Zebra Technologies’ Form 10-K, filed February 13, 2025, discusses on page 4 that key products under its “Automatic Identification and Data Capture” market include “specialty printers for barcode labeling and personal identification… and supplies, such as labels and other consumables.”

20AstroNova “About Us” page as of April 22, 2025. https://www.astronovainc.com/about-us/leadership/

21Michael Natalizia’s LinkedIn page as of April 22, 2025. https://www.linkedin.com/in/mike-natalizia-9571353/ The LinkedIn profile of Andy Ellis, a Regional Sales Manager for AstroNova from 2022 – present and a Field Sales Engineer for AstroNova from 2013 – 2021, cites a prior role as Internal Account Manager at Zebra Technologies from May 2000 – November 2002. https://www.linkedin.com/in/andy-ellis-1135a535/details/experience/ A LinkedIn profile for Jerry Lim, an Asia Sales Leader for AstroNova from October 2014 – Present, cites a prior role as Business Development Manager for Brady Corporation from January 2011 – August 2013. https://www.linkedin.com/in/jerry-lim-71908714/

22All data in table above sourced from YCharts.

232012 Definitive Proxy Statement for Allied Motion Technologies (the former name of Allient). Page 10. “In 1993, he [Mr. Warzala] was named President of API Motion, a subsidiary of American Precision Industries Inc., and continued as President until 1999, when it was acquired by Danaher Corporation where he served as President of the Motion Components Group until 2001.” Additionally, see AstroNova’s FY2025 Definitive Proxy Statement filed May 19, 2025 – page 14. “[Warzala] formerly was … President, API Motion, a division of then publicly traded American Precision Industries until it was acquired.”

24AstroNova’s FY2025 Definitive Proxy Statement filed May 19, 2025 notes: “Prior to Performance Motion Devices, Mr. Woods served as chief executive officer of Control Technology Corp., a manufacturer of industrial computer and software products; and President of API Controls, a division of Danaher.” Page 14. As of April 18, 2025, Woods’ LinkedIn page cited a five-year stint from 1996 – 2001 as “President, API Controls” at Danaher (“Multi-Billion Dollar manufacturer of Industrial, Medical, and Scientific equipment (NYSE: DHR). Acquired by Danaher in 1999”). https://www.linkedin.com/in/gregwoods1234/details/experience/ A copy of Mr. Woods’ LinkedIn page as it appeared on 2025-04-17 has been saved. American Precision Industries’ Form 10-K for the Fiscal Year ended December 31, 2008, notes that API Controls is a division of API Motion; the document makes three references to Richard S. Warzala https://www.sec.gov/Archives/edgar/data/5657/0000950152-99-002859.txt

25For Mr. Michas, reference 2015 – 2017 proxy statements from Allied Motion Technologies. For Mr. Warzala, see page 14 of AstroNova’s FY2025 Proxy Statement.

26“AstroNova Sends Letter to Shareholders Highlighting Growth Strategy and Strength of Board.” May 19, 2025. https://investors.astronovainc.com/news/press-releases/press-release-details/2025/AstroNova-Sends-Letter-to-Shareholders-Highlighting-Growth-Strategy-and-Strength-of-Board/default.aspx

27AstroNova Form 10-K for FY2014 filed April 7, 2014. Page 18.

28See above. Page 57.

29Form 10-K for FY 2025, filed April 15, 2025.

30Miltope: see FY2014 Form 10-K filed April 7, 2014 – page 19. RITEC: see FY2016 Form 10-K filed April 8, 2016 – page 20. TrojanLabel: see FY2018 Form 10-K Filed April 10, 2018 – page 54. Honeywell: see FY2018 Form 10-K filed April 10, 2018 – page 52. Astro-Machine: see FY2023 Form 10-K, filed April 17, 2023 – page 25. MTEX: see FY2025 Form 10-K, filed April 15, 2025 – pages 13 and 15.

31Astro-Machine Acquisition Presentation, August 9, 2022.

32See footnote 18.

33Form 10-K for FY 2025, filed April 15, 2025, 2025-04-14 8-K Result of Operations

34See footnote 26; all data in this section sourced from these disclosures by AstroNova.

35Ibid – see footnotes 32 and 33.

36Form 10-K for FY 2025, filed April 15, 2025: “MTEX had an operating loss of $16.9 million on revenue of $42. million. MTEX’s operating loss includes a $13.4 million charge related to goodwill impairment.”.

37“Former SVP at Memjet Believes AstroNova Needs Clear Marketing Strategy for Growth and Profitability.” Tegus – May 15, 2025.

38Form 10-K filed April 12, 2024.

39Q4 FY2022 Earnings Call Transcript – April 22, 2014. CEO Greg Woods: “the solution has been put in place and kind of putting that behind us.”

40AstroNova Sends Letter to Shareholders Highlighting Growth Strategy and Strength of Board.” May 19, 2025. https://investors.astronovainc.com/news/press-releases/press-release-details/2025/AstroNova-Sends-Letter-to-Shareholders-Highlighting-Growth-Strategy-and-Strength-of-Board/default.aspx

41Q4 Earnings Presentation, Page 8. April 14, 2025.

42TCS Digital Solutions, a distributor of products from Afinia, TrojanLabel, Quicklabel, Epson, and others, notes. “The lifespan varies but typically ranges from 3-7 years depending on usage and maintenance. Maintaining your printer is essential to its longevity.”https://tcsdigitalsolutions.com/color-label-printers/ While exact lifespans depend heavily on the specific product, its usage, and its maintenance, our research leads us to believe that this is a reasonable estimate to use at a high level.

SOURCE: Askeladden Capital Management LLC

View the original press release on ACCESS Newswire